Why the Traditional Financial Advisor Fee Model Works Against You

Most financial plans are designed to guide long-term decisions, often spanning decades. Yet the most common financial advisor fee model charges clients every single year, regardless of whether their financial plan actually changes.

This mismatch is one of the biggest—and least discussed—problems in the financial advisory industry.

Under the traditional assets under management (AUM) fee model, investors typically pay around 1% of their portfolio annually. As assets grow due to market returns, ongoing savings, or both, the advisory fee automatically increases. The advisor earns more—not because additional work is being done, but simply because the portfolio balance is higher.

If your financial plan remains largely the same, should your advisory fee keep rising?

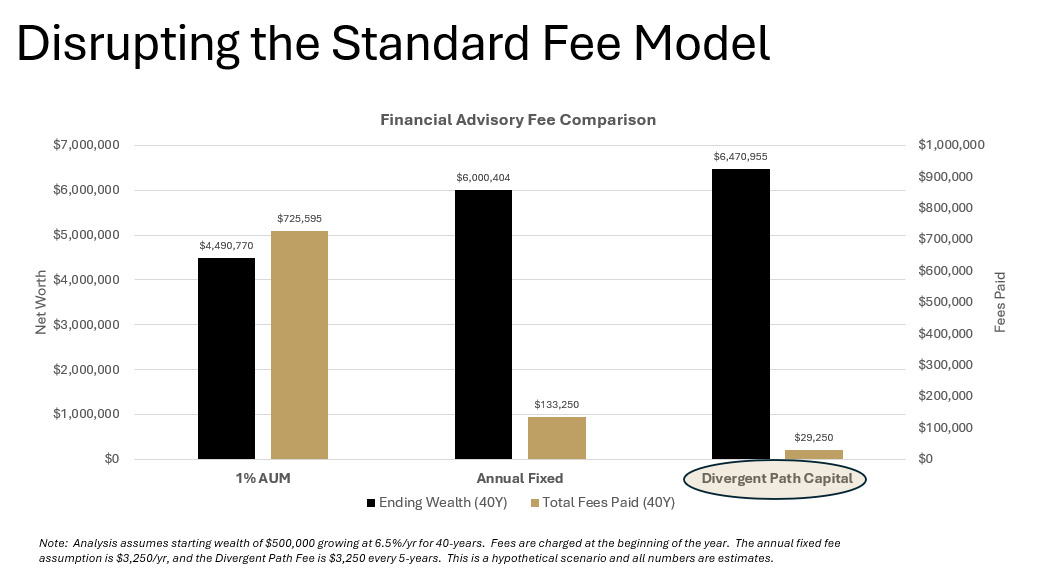

Divergent Path Capital was built to challenge a fee model that charges more without doing more. The chart above illustrates how traditional advisory fees compound against investors—and how our flat, episodic approach changes the outcome.

How Financial Advisory Fees Compound Over Time

The chart above illustrates how different financial advisor fee structures impact long-term wealth over a 40-year period. The assumptions are straightforward:

Starting portfolio: $500,000

Annual return: 6.5%

Time horizon: 40 years

Fees charged at the beginning of each year

We compare three models:

A traditional 1% AUM fee

An annual fixed-fee advisor (membership model)

Divergent Path Capital’s flat, episodic fee model

Each model shows:

Ending portfolio value after 40 years

Total advisory fees paid over the same period

Key Takeaways from the Fee Comparison Chart

AUM fees compound negatively.

Under a 1% AUM model, total advisory fees exceed $700,000 over 40 years—money that no longer compounds for the investor.Higher fees directly reduce long-term wealth.

Even small annual fees can lead to significantly lower ending portfolio values.Membership models can also be costly.

Many years require little to no change in a well-constructed financial plan, yet fees are still charged.Episodic fees are only charged when the client experiences a life change and requests an update.

No new fees are charged unless the financial plan needs to be re-worked

Why the AUM Model No Longer Makes Sense for Many Investors

The AUM fee model was built for a different era—one where financial planning tools were scarce, portfolios required constant manual oversight, and transparency was limited.

Today, technology handles much of the portfolio management process. What investors actually need is high-quality financial planning at key life moments, not perpetual asset-based billing.

The Divergent Path Capital Fixed Fee Approach

At Divergent Path Capital, we believe investors should pay for financial planning work, not asset growth.

Our model is simple:

A fixed fee to build your financial plan

No ongoing advisory fees if your plan doesn’t need updating

Lower follow-up costs when life changes require adjustments

If nothing changes, you shouldn’t keep paying.

When your life does change—career shifts, family milestones, retirement planning—we step in with targeted planning updates. Because the foundational work is already done, follow-up fees are typically lower.

Final Thoughts on Financial Advisor Fees

Financial planning should be long-term and intentional. Your financial advisor fee model should reflect that. Reducing unnecessary advisory fees isn’t about cutting corners—it’s about keeping more of your money working for you over time.

If you’re questioning whether your current advisor’s fee structure aligns with your actual needs, you’re asking the right question.